Capital Gains

Capital Gains Tax Exemption

Capital gains tax occurs when selling personal and investment real estate property if there is a gain on the sale. You are taxed on the profit you gain from the item’s sale over your original purchase price. The IRS form to file for capital gains is Schedule D.

Your primary residence is exempted from the capital gains tax under Section 121 of the tax code. If the following criteria are met, you can exclude up to $500,000 of your gain if you are married and filing jointly and up to $250,000 if you are filing singly.

- The taxpayer must use the property as a principal residence for two out of the last five years before the sale.

- The use as a principal residence does not need to be in concurrent months.

- The §121 exclusion is only available once every two years.

- Second homes and vacation homes do not qualify for §121 tax exclusion.

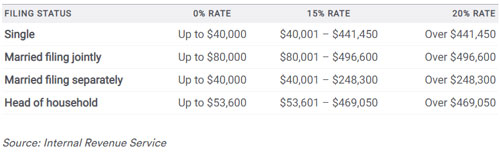

The amount you gain after these thresholds gets the capital gains tax applied. Here are the current long-term capital gain tax rates:

3 Tips on How to Reduce Capital Gains Tax Legally

#1 – Deduct Closing Costs

You can deduct all closing costs from the capital gain to help reduce the taxable balance. If, after applying your exemption amount, there remains a capital gain, be sure to deduct all closing costs to reduce your taxable capital gain amount further.

Closing costs that you can deduct typically include

Title Insurance, Escrow Fees, Commissions, Taxes, and Recording Fees. Qualified closing costs include any fee that covers expenses needed to close the sale transaction.

#2 – Apply the exemption amount.

Subtract your exemption amount from the capital gain. Example #1 – A married couple sells their home for $1,300,000. They deduct the married filing jointly capital gains exemption of $500,000 from the capital gains amount. They also deduct what they originally paid for the property ten years ago: $700,000. This brings their taxable amount to $100,000.

#3 – Deduct improvements that you invested in the home being sold.

Deduct major improvement items from the capital gain amount. The IRS defines allowable improvement items as a home improvement that adds market value to the home, prolongs its useful life, or adapts it to new uses. For example, room additions, new decking, roof replacement, new HVAC, new wood flooring, kitchen remodel, and bathroom remodel all qualify. Do not include minor repairs such as paint, lighting fixture replacement, or other similar minor items.

Example – Bob and Mary from Example #1 remodeled their kitchen and master bathroom five years ago. It cost them $80,000. They subtracted these significant remodel costs from their remaining capital gains of $100,000. Their new capital gains taxable amount is $20,000.

Income Qualification

Another consideration for your CPA to work out with you is your income qualification. If your single income is $40,000 or less or your married income is $80,000 or less annually, you are exempt from the capital gains tax. This income includes income after personal business expenses are deducted.

City and County Property Tax

Ensure your closing title company properly accounts for the prorated city and county taxes. This will ensure that the seller pays the city and county property taxes only up until the closing date and the buyer pays those taxes from the closing date.

The escrow company will ensure that each party calculates those pro-rated amounts correctly. Unfortunately, there is no way of getting out-of-city and county property tax for either party unless the sales agreement stipulates that the buying party will pay all due property taxes. A purchase agreement can specify this as an added incentive to close the deal. In that case, the buyer will pay all property taxes currently due in addition to post-closing.

Property Tax City Chart

2024 Property Tax Rates for Williamson County, TN

2022 Property Tax Rates for Davidson County, TN

The 2022 tax rate for Urban Services District is $3.254, and the rate for General Services District is $2.922. Residential property tax is based on the assessed value, which is 25% of the appraised value, and commercial property tax is also based on the assessed value, which is 40% of the total appraised value.

State Deed Tax

Tennessee imposes a recordation tax on all transfers of real property, with certain exceptions, for recording the instrument that evidences the transfer (e.g., deed, decree, etc.). The tax is based on the consideration for the transfer or the value of the property transferred, whichever is higher, and is 37 cents for every $100. The person who receives the property is responsible for paying the tax to the county register.

Tennessee also imposes a recordation tax on the recordation of any instrument of indebtedness (e.g., mortgage, deed of trust, lien on personal property (other than motor vehicles), etc.), with certain exceptions. This tax is 11.5 cents for every $100 of the indebtedness but does not apply to the first $2,000 of the debt. The debtor pays the tax to the county register or the Tennessee Secretary of State.

For more information on Tennessee’s recordation taxes, see Tenn. Code Ann. § 67-4-409.

Sell House Tax

There’s no getting out of taxes when buying or selling property. It comes along with the privilege of being a property owner. Remember that much of the tax goes to the city to help improve infrastructure and public services. It’s your contribution to the community.

Be smart and buy and sell real estate in a way that makes the most financial sense. Take advantage of these sell-house tax deferrals when you can. Plan to save money.

Disclaimer: the best way to lower your taxes is to review your finances with a CPA tax professional. This article offers tips and information about capital gains tax only. Review your unique financial situation with your tax advisor to help avoid paying unnecessary taxes when selling your house while staying compliant.